You can’t see it or touch it, but a powerful financial tool exists within your home. What is it? No, not the ghost of your long-lost rich ancestor. It’s your home equity!

As fall approaches, “change” is in the air. Cooler weather draws us indoors and shifts our focus from carefree summer days to end-of-year goals like nailing down home improvements, knocking out high-interest debt, or tackling significant expenses before the year wraps up.

Your home equity can help you accomplish all these autumnal achievements. When tapping into it, you have two popular options:

So, what’s the difference? And which one is right for you? Let’s break it down so you can embrace the season and make a financial change for the better.

What is Home Equity?

To start, home equity is your home’s current market value minus the amount you owe on a mortgage.

When the value of your home increases, and the amount you owe on your mortgage decreases, your home equity rises. More home equity means more collateral for achieving goals through methods such as loans, cash-out refinances, or selling your home.

What Is a Home Equity Loan?

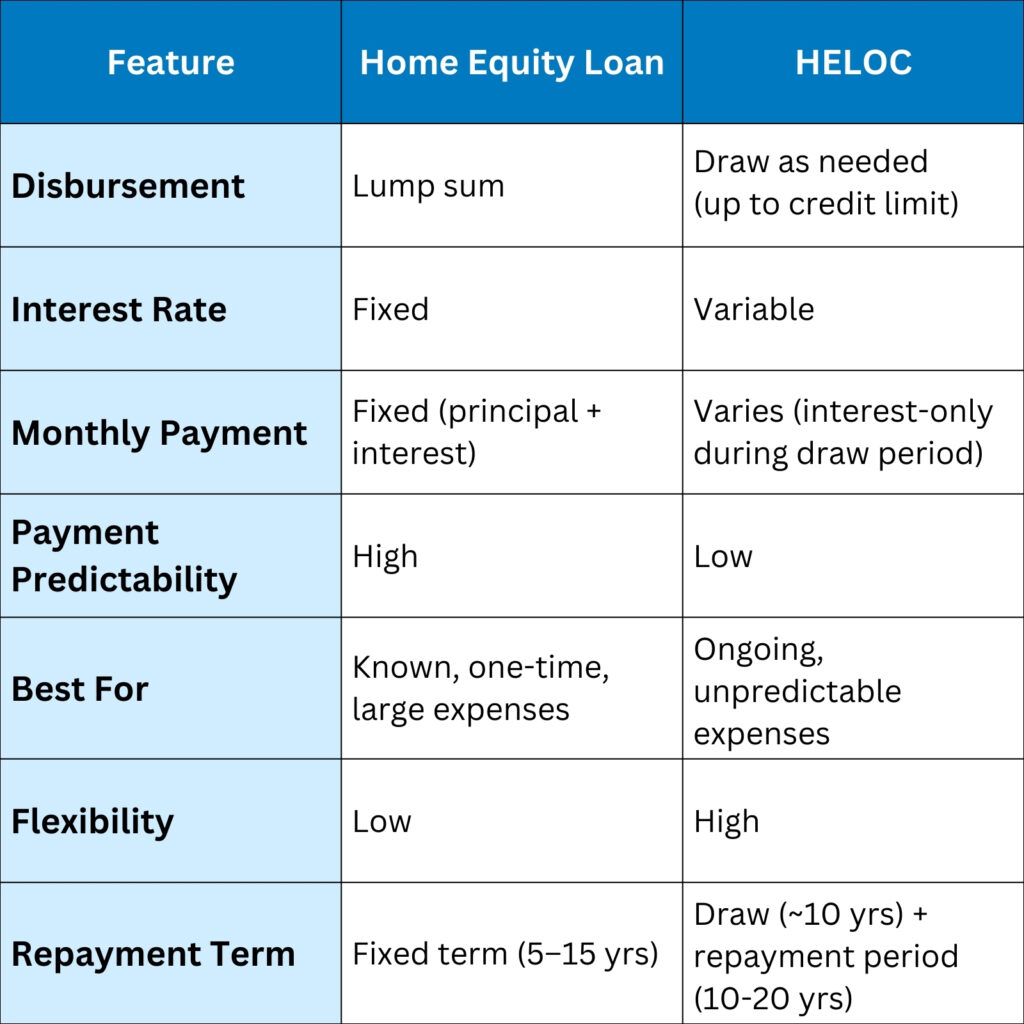

A Home Equity Loan (often called a second mortgage) gives you a lump sum of money upfront, which you repay over a set term with fixed monthly payments and a fixed interest rate. The term “fixed” means they do not fluctuate.

Best for:

- One-time expenses (e.g., home renovations, medical bills, tuition)

- Those who want predictable payments and a fixed rate

Pros:

- Fixed rate = stable monthly payments

- Ideal if you know the exact amount you need

- Terms typically range from 5 to 15 years

Cons:

- Less borrowing flexibility

- Higher initial monthly payments compared to HELOCs

What Is a HELOC?

A Home Equity Line of Credit (HELOC) works more like a credit card. You’re approved for a maximum amount you can borrow, referred to as your credit limit, and can draw funds as needed during a set draw period, usually 10 years. During the draw period, you only pay interest on what you use. However, HELOC interest rates are typically variable, meaning they can fluctuate.

After the draw period, you enter the repayment period, usually 10 to 20 years. During this time, you repay both interest and the amount you borrowed, referred to as your principal. You can no longer borrow funds from your credit line during this time. While it’s possible to pay off your HELOC before your draw period ends, some lenders charge an early repayment penalty.

Best for:

- Ongoing or unpredictable expenses (e.g., phased home projects, emergency funds)

- Borrowers who prefer flexibility

Pros:

- Flexibility to borrow as needed

- Interest-only payments during the draw period

- Reusable line of credit (borrow, repay, and borrow again)

Cons:

- Fluctuating interest rates that alter payment totals

- Riskier for people who struggle to control spending and borrowing

How Do They Compare?

Which One Is Right for You?

If you prefer predictability and have a specific expense in mind, a Home Equity Loan may be your best bet. For example, if you know for a fact that your window replacement will cost $5,000, a home equity loan could be wise because you know exactly how much money you need and when you need it.

If you value flexibility and want access to funds over time, a HELOC could be the way to go. For example, during a lengthier project like a kitchen renovation, you may encounter unexpected changes that require more or less money and time. A HELOC is designed for such flexible needs.

Next Steps

At 1166 Federal Credit Union, we offer both options with competitive rates and fewer fees than the big banks. You’ll find NO upfront application costs on home equity loans or HELOCs, and our home equity loans have a flat $900 closing fee, unlike other financial institutions that charge high percentages of your total loan amount. Plus, our lending team is here to help you choose the right fit for your goals. Contact us to get started!