Anyone else plagued by HATAT syndrome: How Are They Affording This? It’s the thought that hits the moment I scroll through someone’s vacation photos on Instagram, along with “take me with you!”

If you’re tired of FOMO and want a summer trip that doesn’t trip up your finances, here’s how to do it without paying the price long after you’re home.

Not All Who Wander Can Afford It

The average one-week vacation in the U.S. costs about $2,000 per person, and more than half of U.S. adults plan to take a vacation this year. Yet, nearly 29% of these vacationers expect to go into debt to fund their trips.

So that “How are they affording this?” question?

Well, a lot of times…they’re not. They’re just delaying the cost.

Debt Reality Check

It’s easy to swipe now and deal with it later, but vacation debt doesn’t disappear when the trip does.

Put $500 on a credit card with 21% interest and pay $50 a month, and you’re looking at about a year to pay it off. That’s 12 months of future income paying for a past vacation.

Debt isn’t a travel plan; it’s a financial leech disguised as a martini by the pool.

The B-Word (It’s Not What You Think)

Before you plan anything, know what you can actually afford. Yes, we’re talking about the b-word (a budget), but not the restrictive, no-fun kind. One that shows you what’s possible!

When you look at your income, expenses, and account balances, you’ll find your discretionary income: the money left after essentials (groceries, bills, mortgage, etc.) are covered. That’s where your vacation fund should come from, not from money already spoken for.

Build a Vacation Savings Plan

Once you know what you can realistically set aside, build a simple savings plan to eliminate any vague cross-your-fingers-and-hope-it-works-out saving efforts.

Treat your vacation like any other expense and contribute to it consistently. This spreads the cost out over time instead of forcing a last-minute scramble.

For example:

- Trip cost: $2,000

- Time to save: 12 months

- Monthly savings: $167

- Per paycheck (2 per month): about $83

Now you have a plan!

Set Your Vacation Cap

If you’ve budgeted $2,000 for travel this year, that’s your cap. Every decision should ladder up to that number. If your dream trip exceeds that cap:

- Adjust the trip

- Or extend your timeline and save more

What you don’t do is force it with debt.

Build Your Vacation Budget

Once you’ve set your cap, break it down into a working vacation budget, including fixed and variable costs such as:

- Transportation (flights, gas, parking, rideshares)

- Lodging

- Food (main meals AND quick stops)

- Insurance

- Activities

- Souvenirs

- A buffer (aim for 15–25% for the unexpected)

This isn’t about restriction, it’s about spending with confidence. When you eliminate guesswork, your expenses feel just as good in the moment as they do when the bills roll in.

Pro Tip: Use travel rewards or cashback where you can to reduce out-of-pocket costs.

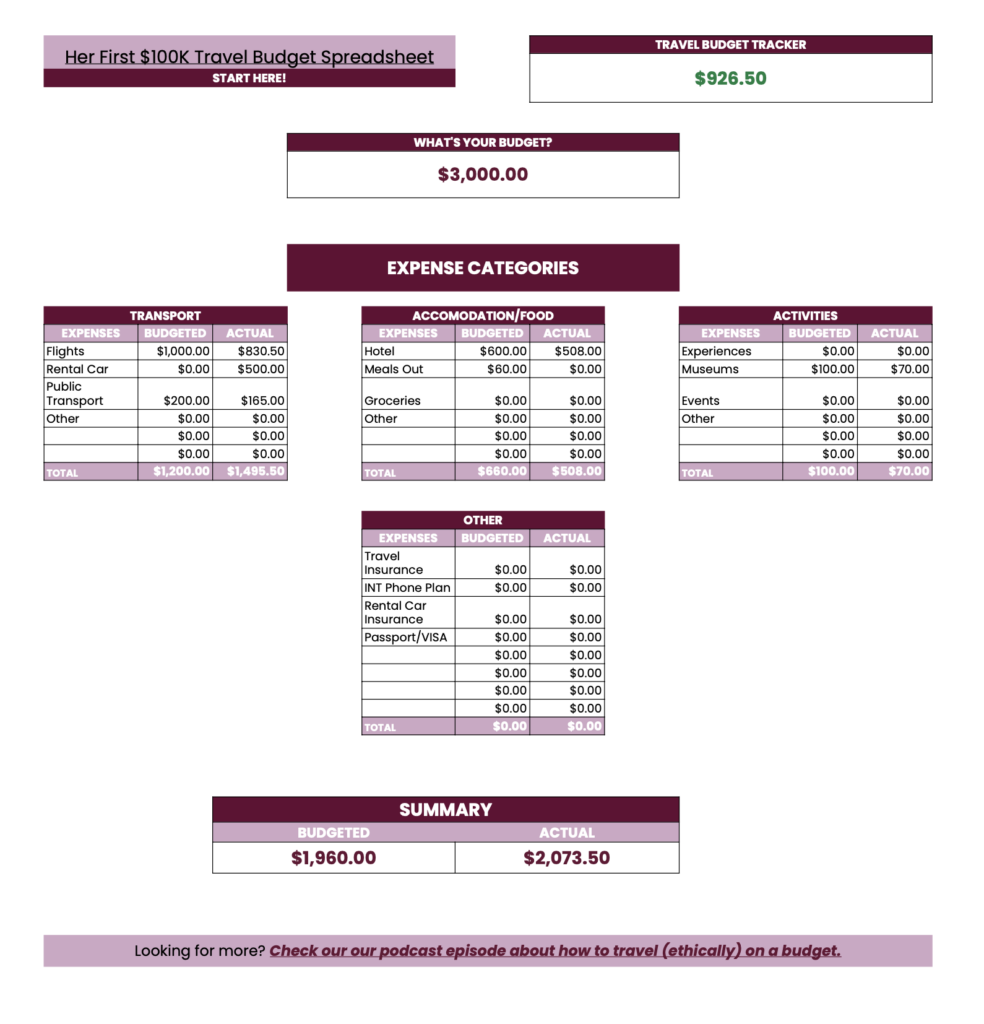

Check out this free Travel Budget Spreadsheet created by Her First $100k to get you on the right track!

Flexibility is Key

If you’re open to where you go and are more focused on having a great experience rather than a trip to a specific destination, you have a huge cost-saving advantage on your hands.

Instead of locking in on an expensive plan:

1.) Compare destinations based on cost:

2.) Travel off-peak or mid-week

3.) Prioritize personal interests and desired activities over tourist destinations

4.) Look for the deals first and then decide

The more flexible you are, the more options you have, and the more money you can save.

And if you’re set on a specific trip that’s currently out of financial reach, that’s when you adjust your savings plan to get there in the future rather than forcing it to happen now.

Sinking Fund to Stay Afloat

Where you keep your vacation money matters.

A sinking fund is a savings account for upcoming, planned expenses like vacations or car payments, that keeps the money separate from everyday spending.

Storing your sinking fund in a high-interest-earning account helps your savings grow. With no extra effort, this makes it easier to reach your goal.

Here are some smart options for where to keep your sinking fund:

High-yield savings account (HYSA)

- Earns higher interest than a traditional savings account

- Automatic deposits from paycheck

- Low risk and easy access

Time deposit account or CD (Certificate of Deposit)

- Keeps money locked up for a fixed term (3 months…1 year…etc)

- Less temptation to spend savings due to early withdrawal fees

- Predictable returns (you know exactly how much interest you’ll earn by the end)

Money market account

- Earns higher interest than a traditional savings account

- Flexible withdrawals (check-writing or debit access)

- May require a higher minimum balance

Bonus: New PhilaPort Cruise Terminal

If you’re in the Philly area, you’ve probably heard the buzz around the newly opened PhilaPort Cruise Terminal. And while this isn’t a pitch to book the next ship out, it is worth noting for travelers looking to make the most of their vacation budget.

Through the port’s partnership with Norwegian Cruise Line, you can now sail to destinations like Bermuda, the Caribbean, and Canada right from your backyard. With cruise packages like “Free at Sea,” travelers can bundle perks such as open bars, specialty dining, Wi-Fi, and excursion credits into a single upfront cost. It’s these kinds of inclusions that can make cruises a surprisingly efficient option for travelers who want more experience with less spending and planning.

The Bottom Line

You should come home from vacation with great memories, not debt.

With a little planning, a clear limit, and some consistency, you can enjoy your trip and your finances post-vacation.

How 1166 FCU Can Help

Everyone deserves to enjoy their upcoming vacations without sacrificing their finances. Contact us today for financial guidance, useful resources, and tools to help you make informed decisions and reach your goals.