Here’s a new take on slimming down for summer, and it doesn’t involve Tai-Chi walking! As auto purchase prices have climbed from an average of $34k to $50k in the past decade, purchasers are now seeking value over luxuries. And, with gas prices rising, they are also opting for smaller, fuel-efficient SUVs and trucks over larger models.

If you’re considering ways to cut down on your transportation costs, here’s the skinny on auto loans.

What is an auto loan?

Auto loans save the day for vehicle purchasers who prefer not to or don’t have the cash to pay the full cost of a vehicle up front. Instead, a lender provides the funds to purchase the car, and the borrower repays the loan over time through monthly payments that include principal, interest, and sometimes additional add-ons, such as insurance.

These “fixed” monthly payment amounts stay the same throughout the loan term, which is usually 36 months to 60 months. If you stop making payments on the loan, you may find yourself left out in the sun, as the lender can repossess the car.

Who does an Auto Loan Help?

While you may have stashed away enough cash for a stormy summer day, most vehicle purchasers need a little help to get new wheels on the road. An auto loan helps:

- Those With Less Purchasing Power

Young adults, recent graduates, and individuals on a tight budget… whatever your reason for not being able to buy a car outright, auto loans can help make the process easier. However, auto loans are not a green light for living beyond your means when it comes to vehicles. An auto loan is intended to financially assist you, not have you building your future on sinking sand.

- Individuals with less credit history

Being responsible with your repayment schedule reflects positively on your credit score. If you’re looking to build your credit history, an auto loan can help you diversify your credit mix.

- Those who want to keep their money in savings accounts

An auto loan helps you keep your money in interest-earning accounts, such as a high-interest savings account or investment account. As these funds remain accessible, they increase your security in the event you experience an emergency, like the kind that roll in unexpected on a steamy summer night.

What should I know about Auto Loans?

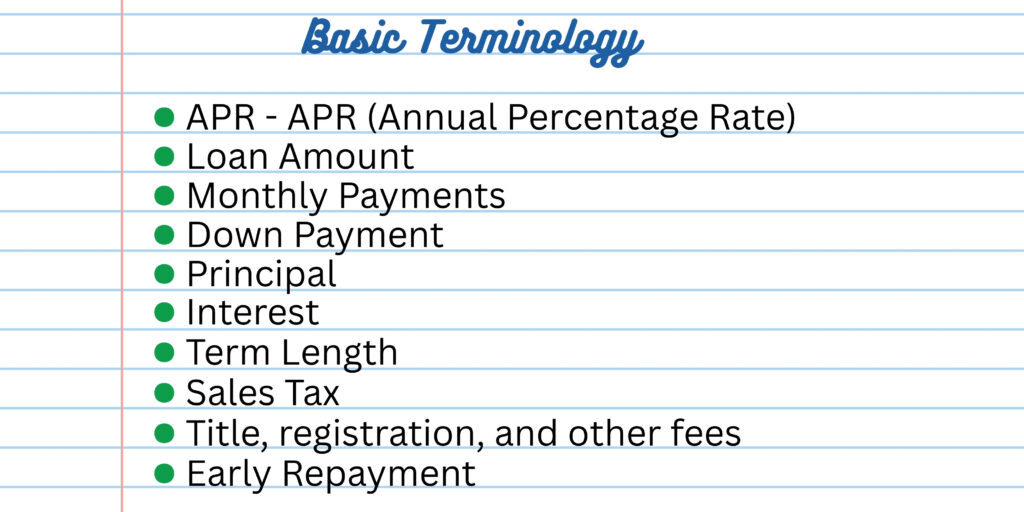

Knowing the basic terminology puts you in the driver’s seat in the search for the best deal. Consider:

- APR – APR (Annual Percentage Rate) is the yearly cost of borrowing money for a car, including interest and most associated fees, expressed as a percentage. It provides a more accurate picture of loan costs than just the interest rate.

- Loan Amount – The total amount of money you borrow to purchase a car.

- Monthly Payments – The amount you pay each month on your loan, including principal and interest. Extra payments can reduce the loan term and total interest paid.

- Down Payment – The amount paid upfront or via trade-in to reduce the loan balance. A larger down payment lowers monthly payments and total interest.

- Principal – A portion of your monthly payment that repays the original amount you borrowed.

- Interest – A portion of your monthly payment that is charged as a percentage of your loan balance for borrowing money. Borrowers with higher credit scores usually qualify for lower interest rates.

- Term Length – The period you have to repay the loan, typically 36–72 months. Shorter terms often have lower interest rates but higher monthly payments.

- Sales Tax – Most states require a sales tax for auto purchases, which will be factored into the purchase of your vehicle with the loan.

- Title, registration, and other fees – These fees are collected by the dealership or the state for vehicle registration, processing, and legal documentation.

- Early Repayment – Paying extra toward your loan each month can shorten its term and save on interest. Some lenders may charge a penalty, but 1166 FCU does not.

That’s a lot to consider, but you don’t have to figure it all out on your own. With this convenient auto loan calculator, you can easily estimate your loan payments without breaking out in a sweat!

Where Can I Get an Auto Loan?

While dealerships, banks, online lenders, and credit unions all offer auto loans, not all offers are the same.

- Dealership financing offers the convenience of a one-stop shop where buyers can choose a car, secure financing, and complete the purchase in one place. Dealerships may also work with a network of lenders that have different qualification requirements, and brand-specific financing companies sometimes provide rebates or attractive promotional rates. However, dealership financing often comes with higher interest rates, sales pressure, and upselling tactics. Loan terms may also be longer, buyers are limited to the dealership’s inventory, and it can be more difficult to compare the true cost of loans across different dealerships.

- Bank financing allows buyers to shop around for the best loan rates and terms before purchasing a vehicle. Getting pre-approved through a bank can help avoid dealer add-on pressure and save time during the purchase process. Bank loans can typically be used at franchise dealerships, independent dealerships, and with private sellers, and existing customers may receive additional perks or discounts. On the downside, buyers may miss out on special dealer promotions, the process can be slower than dealer financing, some banks may only work with approved dealerships that have higher rates, and qualification requirements are often stricter.

- Online lenders provide a quick and convenient approval and application process, making it easy for buyers to compare rates from multiple lenders. They are generally accessible to borrowers with a variety of credit histories and offer flexibility in financing options. However, online lenders may provide less personalized customer service, and borrowers should be cautious about privacy risks, scams, and hidden fees. Interest rates can also vary significantly between lenders.

- Credit unions are often known for offering some of the lowest interest rates because they operate as member-owned institutions. Their financing can usually be used at franchise dealerships, independent dealerships, and with private sellers. Credit unions also tend to be more flexible with borrowers who have limited credit history or experience, while offering personalized service, lower fees, and more flexible repayment terms. The drawbacks include membership requirements, fewer physical branch locations—although many offer online approval—and the possibility of missing out on special dealer financing promotions. In addition, the approval process may take longer than dealership financing.

At 1166 Federal Credit Union, we care about our members’ finances and the impact that increased gas prices are having on their budgets. That’s why we’re shrinking our Auto Loan rates from 4.25% to 4.0% through July 2026.

If you’re ready to slim down your high gas bills this summer and sunset your less-efficient vehicle for a new or used ride with lower payments and better mileage, reach out to us for a fee-free auto loan application and fast pre-approval process.